Complex retirements

Select an article to discover more

This is for investment professionals only and should not be relied upon by private investors.

need straightforward expertise

Flexibility and certainty: Achieving both in retirement through integration

Long overlooked, the concept of combining annuities and drawdown in a single retirement plan is starting to gain traction

Read more

Closing the retirement readiness gap: The adviser's role

The journey to retirement is not solely a financial one; it's deeply intertwined with a client's psychological readiness. For financial advisers, navigating this complex landscape is key to shaping clients’ futures

Retirement strategies

Planning an income in retirement is far from straightforward. Here we present some ideas and analysis on how clients can successfully navigate a life stage that can last 30 years or more

Video: Autumn Budget 2025 – beyond the headlines

Join Fidelity Adviser Solutions’ experts as they unpack the key Budget announcements and their practical implications for financial advisers

Select a previous article

A snapshot of the 2025 Budget

Even though the November 2025 Budget was probably one of the most leaked and trailed events in history, there were still one or two surprise announcements in the Chancellor’s Statement

Adaptive retirement advice: from cliff-edge to course correction

How advisers keep relationships strong when time is the scarcest resource

Retirement readiness: Understanding client behaviour

How changes in IHT treatment will impact retirement savers

Tackling the nemeses of a comfortable retirement

In partnership with

Fidelity Adviser Solutions

Watch video

Important information Issued by Financial Administration Services Limited, authorised and regulated by the Financial Conduct Authority. Fidelity, Fidelity International, the Fidelity International logo and F symbol are trademarks of FIL Limited. UKM0825/404983/SSO/0826

Back to the top

Today’s non-linear retirements require a different approach

Video: Retirement strategies

Does emotional intelligence offer advisers an edge?

What are the needs at each stage of a retirement journey?

The psychology of retirement

Bridging the advisers-clients gap: How emotional intelligence can help build deeper trust with clients and better understand their financial goals

For some clients, the first day of retirement may feel less like freedom and more like free fall. Despite years of planning, the sudden loss of structure and professional identity can trigger anxiety and uncertainty. This is a sign that retirement is not just a financial event but a psychological one. Increasingly, advisers find themselves acting as retirement coaches, supporting clients through the emotional transitions that accompany this life stage, alongside the technical aspects of financial planning. “A key non-financial issue is that our identities are very strongly tied to work,” explains James Woodfall, Communication and Behaviour Specialist at Raise Your El. “When clients transition into retirement, they lose part of that identity.” Woodfall, a former financial planner, now works with firms to incorporate emotional intelligence into advice processes to improve company performance. He notes that the disruption to long-standing routines, often structured around work, can leave clients struggling. The need to re-establish internal schemas, routines, and behavioural cues presents a psychological challenge not just for clients, but for the advisers supporting them. “As advisers, we’re not formally trained to help people through this transition,” Woodfall continues. But in many cases, advisers may be the only professional clients speak to about the psychological aspects of retirement.

“Research suggests that people take around three years to adjust psychologically to retirement,” Woodfall explains. During this time, advisers have a crucial role to play in preparing clients, not just financially, but behaviourally. For example, encouraging clients to visualise a typical post-retirement day or week can be useful. One adviser Woodfall worked with even encouraged a client to role-play a social event, rehearsing how they would introduce themselves without a job title. “This helped the client establish the mental and emotional foundations needed to navigate retirement more confidently,” Woodfall adds. Where a phased or gradual retirement is possible, the transition tends to be smoother. In contrast, “cliff-edge” retirements - when clients stop work abruptly - can be destabilising. “It’s too much change, too quickly, without time to prepare for the future,” says Woodfall.

Meanwhile, there’s often a gap between how clients imagine retirement and the lived experience. While many anticipate relaxation and leisure, the absence of structure can quickly lead to boredom, loss of purpose, and social isolation. “Experience updates the plan,” says Woodfall and advisers are well-positioned to help clients recalibrate as they test assumptions and uncover what retirement really looks like. Key questions to explore with clients may include:

Retirement expectation versus reality

“People take around three years to adjust psychologically to retirement. During this time, advisers have a crucial role to play in preparing clients, not just financially, but behaviourally”

Understanding the retirement timeline

• How will you structure your time daily and weekly? • What roles or activities will replace work as sources of meaning or purpose? • How do you want to feel in retirement, and what supports that?

Drawing on case studies or anonymised examples from other clients can help normalise these discussions and add depth to planning conversations.

Saving for retirement versus spending

For some clients, anxiety may be focused on spending in retirement, especially after decades of saving for homes, education, or retirement itself. “Don’t underestimate the power of the saving habit,” Woodfall warns. He shares the example of a client who, despite selling a business for over £20 million, became extremely frugal in retirement due to fear of running out of money. “Emotion takes over and can override logic,” he explains. To counteract this, advisers may want to implement new behavioural strategies, such as simulating a salary through regular drawdowns, to ease the psychological transition. And to help develop the adviser-client relationship, it is also essential to acknowledge client concerns empathetically. “If a client says they’re worried about running out of money, don’t say ‘That’s silly, you’ve got £20 million.’ Dismissing fears undermines trust. Our job is to flex to the client, not expect them to flex to us.”

Retirement coaching

Advisers already use many tools to support clients through the non-financial aspects of retirement. Behavioural coaching frameworks can add further structure and depth, such as Martin Seligman’s PERMA model – Purpose, Engagement, Relationships, Meaning and Achievement. Combined with life-timeline exercises, it can prompt reflection on formative experiences and spark ideas for fulfilling activities in later life. Technical planning tools also play an important role. Modelling “phased retirement” - reducing workdays over several years – can soften identity and routine disruption. Incorporating “pre-mortem” planning into cashflow models allows advisers to stress-test against market volatility, longevity risk, and major expenses, then develop mitigation strategies in advance. As one of life’s biggest transitions, not just financially, but psychologically and emotionally, advisers who understand and support clients through retirement changes offer significantly more value than those who focus solely on the financial numbers. And by combining technical planning with behavioural insight and empathy, advisers play a critical role for clients.

“Incorporating “pre-mortem” planning into cashflow models allows advisers to stress-test against market volatility, longevity risk, and major expenses”

James Woodfall Communication and Behaviour Specialist, Raise Your El.

Complex retirements need straightforward expertise

Return to home

Further reading

Discover more from Fidelity on how emotional intelligence can foster better client relationships.

In association with

The financial needs of retirees change dramatically from one phase to the next. From accumulation and protection to resilience and stability, retirement planning must also evolve to align with the individual’s needs

Retirement today happens in multiple stages — each requiring a tailored approach to income, risk, and lifestyle. From capital growth and risk reduction to flexible income and longevity protection, modern pension strategies should be adaptable to the retiree’s individual journey. “The accumulation stage is quite simplistic – it's about trying to turn income into as much capital as possible,” says Paul Squirrell, Head of Retirement and Savings Development at Fidelity. “If you're starting your retirement saving in your early 20s, then risk is largely irrelevant because you've got a long term.” But as retirement draws closer, things change. “You’ve got that risk zone when you approach retirement” he says — a phase where exposure to market losses can be much harder to recover from.

In the five to ten years before retirement, priorities begin to shift from accumulation to preservation. “The first thing is to establish what you intend to do in retirement and plan in advance,” says Squirrell. “For me, what is absolutely crucial is identifying the intended process as early as possible,” he says. This helps determine asset allocation, risk exposure, and whether income guarantees may be appropriate. “For example, if I’m going to annuitise in the lead-up to retirement, then it’s essential to preserve the capital – so the usual approach would be to go into gilts or cash, or a combination of the two,” he explains. “However, that approach is not sensible if my intention is to go into drawdown because you don’t want to de-risk something that you’re then going to put back into risk for 30 years.” Squirrell adds: “It isn’t a case of getting to retirement then deciding what to do. Planning needs to take place in advance.”

The transition into retirement often includes winding down work, taking partial benefits, or phasing into decumulation. “As you start to reach retirement, it’s a case of identifying risk and aligning it to the timeframes and money that you’re going to need,” says Squirrell. “As people approach retirement, they’re less willing to take risk. They can’t rebuild the income, so what happens if there is a 20% fall in the markets?” he says. “When living on a finite amount of money, the capacity to absorb loss has got to be greater.” One major consideration in this phase is sequence-of-returns risk — poor market performance early in retirement. “Losses plus withdrawals do not go together because what it’s going to do is compound any damage that is done.” Squirrell advises identifying future cash flow needs as early as possible. “If I’ve got an idea of what sort of capital I’m going to need for expenditure, then I can start thinking about reserves.” He also advocates diversification: “Having different options in terms of meeting your income needs is quite important, including from different types of tax wrappers.” This is where bucket strategies can be effective. “Start identifying what’s needed over different timeframes and put the right level of risk against each,” he says. This allows near-term needs to be met with lower-risk assets, while longer-term funds remain invested for growth.

Transition: Reducing sequence risk and building resilience

Paul Squirrell Head of Retirement and Savings Development, Fidelity Adviser Solutions

Pre-retirement planning

Later retirement: Preserving stability and simplifying income

In later retirement, the focus often shifts from maximising returns to maintaining simplicity, security, and peace of mind. Spending may decline, but new pressures — such as care needs or cognitive vulnerability — can emerge. Once again, this is where early planning pays off. “If you haven’t done that analysis right up front, then you won’t know what flexibility you’ve got,” he says. By clearly distinguishing essential from discretionary expenditure earlier in retirement, income can be adapted more easily in response to changing health or lifestyle. Beyond technical planning, Squirrell highlights a vital but often overlooked factor: behaviour. “You can’t underestimate the importance of the psychology,” he says. “Particularly things such as vulnerability.” As clients shift from saving to spending, emotional support and clarity become just as important as portfolio design. “The peace of mind that comes from knowing you’ve got the essentials covered — that’s a big part of it.”

“As people approach retirement, they’re less willing to take risk. They can’t rebuild the income, so what happens if there is a 20% fall in the markets?”

Read more from Fidelity on retirement strategies.

James Woodfall explains why emotional intelligence is a critical skill that enables financial advisers to build trust, navigate client emotions, and deliver better outcomes

Financial advice is often seen as a numbers game – the right asset allocation, the optimal drawdown rate, the tax-efficient strategy. But for James Woodfall, Communication and Behaviour Specialist at Raise Your EI, the real differentiator for high-performing advisers lies in emotional intelligence – the ability to recognise, understand and manage emotions. “Advisers need to offer a great deal of emotional reassurance to clients,” says Woodfall. “From helping them navigate the identity shift associated with retirement, behavioural resistance to spending, and lifestyle changes after leaving work – and often without specific training in these areas.” It is in these moments, he argues, that emotional intelligence becomes not just a helpful trait, but an essential professional skill. And at the heart of that skill is the ability to build, deepen, and sustain trust to support long-term client growth.

For Woodfall, trust is the key currency in adviser-client relationships. A former adviser himself, he knows that trust does not simply appear because of a financial qualifications or years of service. Rather it is earned through how advisers listen, respond, and adapt to individual clients. That process begins with emotionally intelligent communication: listening without bias, showing genuine curiosity, and making the client feel understood rather than hurried toward a pre-packaged solution. He warns that pushing an unsuitable solution to a client can backfire. “If you try to force a solution on someone who is not ready to hear it, they will shut down. It is important to work with what the client is comfortable with, even if it means a slower path to a ‘correct’ answer.” Woodfall emphasises that trust also is not something that is built in the initial stages of a client relationship. It must be maintained to be truly enduring. “Even after a decade with a client, if their fears are dismissed or belittled, the balance in trust will erode.” That is why ongoing sensitivity is essential, from validating concerns, explaining options transparently, and matching the pace of advice to the client’s readiness.

Moreover, a significant part of emotional intelligence is noticing what a client’s behaviour reveals an issue, sometimes more than their words. Hesitation, a shift in body language, or a change in tone may signal discomfort or anxiety. For Woodfall, The skill lies in reading the moment accurately and adjusting the conversation accordingly. Such cues are prompts for a judgement call: is this the moment to explore a subject further, or is it better to hold back and revisit later? “Emotional intelligence is more of an art than a science,” he says. “Push too hard and you risk damaging trust; hold back too much and you might miss something important.” An ability to spot what’s unsaid is particularly important with clients who are cautious about opening up. Some may keep emotions out of the discussion initially, preferring to focus only on numbers.

Recognising emotion in behaviour

Communication and building trust

Cognitive empathy

Empathy is also a key element of emotional intelligence, although it does not always require personal experience. Instead, advisers can draw upon their professional understanding. “This is called cognitive empathy,” says Woodfall. “You may not know what something feels like first-hand, but you can understand it and respond appropriately.” Developing cognitive empathy often comes from both observing and researching how people adapt to change, handle uncertainty, or make decisions under pressure. This understanding helps anticipate emotional reactions and support clients more effectively.

Self-regulation for advisers

Emotional intelligence is also important in managing the emotions of the adviser. They work in a cognitively and emotionally demanding role, yet are expected to project calm and confidence, even in turbulent markets or during difficult conversations. Those with strong emotional intelligence can regulate their own responses, preventing anxiety or frustration from leaking into the interaction. By staying composed, advisers create a sense of stability that clients can lean on, especially when they are feeling unsettled themselves.

Developing emotional intelligence

Role-playing difficult scenarios, studying behavioural cues, and learning from psychology can also develop advisers’ ability to connect. For Woodfall, the formula for success is clear: “Combine technical expertise with empathetic coaching, and you deliver truly holistic advice.”

active listening seeking feedback reflecting on challenging conversations practising adaptable communication.

Emotional intelligence will vary from one adviser to another, but unlike technical qualifications, emotional intelligence isn’t a fixed credential – it’s a skillset that can be developed over time. Woodfall encourages advisers to work on:

“Trust does not simply appear because of a financial qualifications or years of service. Rather it is earned through how advisers listen, respond, and adapt to individual clients”

Discover more from Fidelity on how enhancing your emotional intelligence can help your clients.

Tackling retirement income challenges and finding opportunities

Driven by regulatory reform, demographic changes and evolving client expectations, there has been a significant shift in the complexity of financial advice for both advisers and their providers. As a result, the advisor’s role has become more critical than ever as they face market volatility, ongoing regulatory and tax changes, and the necessity of tailoring advice to the individual’s needs. So how can advisers best approach some key questions they are faced with today? When does retirement planning typically begin? What are the main challenges as a client approaches retirement? Why is cash flow forecasting so important? What impact will policy changes have on pensions and IHT? How are platforms rising to these challenges? Explore these questions and more in the video hosted by Fidelity Adviser Solutions' Paul Squirrell, Head of Retirement and Savings Development, and with insight from and Laura Whetstone, Director at Lathe & Co Wealth Advisers and John Hale, Senior Platform Consultant, Fidelity Adviser Solutions.

Access more on retirement solutions from Fidelity here.

With longevity increasing, experts urge a shift away from the ‘one-size-fits-all’ 4% withdrawal rule, advocating for flexible, personalised strategies tailored to individual needs, risks, and market realities

The 4% rule, developed in the 1990s by William Bengen, suggests a 4% annual withdrawal from retirement savings could last a typical 30-year retirement. But today’s retirees are living longer and have vastly different lifestyles to their ‘90s counterparts. Such differing individual circumstances mean a one-size-fits-all approach is unlikely to deliver the best outcomes in 2025 according to Paul Squirrell, Head of Retirement and Savings Development at Fidelity Adviser Solutions.

“The regulator suggests the starting point for decumulation is to understand an expenditure analysis for the client – assessing their current and future income needs,” explains Squirrell, adding that a blanket 4% rule ignores individualised client factors and is akin to “putting the cart before the horse.” The original rule was based on a 50:50 balanced portfolio of US stocks and US government bonds, which is overly simplistic for today’s clients and markets. “It’s a mathematical equation,” he adds, noting it may not account for inflation, tax, investment charges and more. “Individuals’ income and capital needs will be very different. Should somebody aged 55 and at low risk and somebody at 65 years of age and higher risk use the same percentage withdrawal strategy? Absolutely not.”

One risk of fixed withdrawal strategies is sequence-of-returns risk – the impact of poor market performance early in retirement. Squirrell stresses that retirees can no longer replace lost income through work. To address this, clients should consider reserving assets for short-term spending needs. “If I’ve got an idea of what sort of capital I’m going to need for expenditure, then I can start thinking about reserves,” he explains. Holding sufficient cash or low-risk investments can help clients ride out market volatility without having to sell down core assets at depressed values. This preserves portfolio longevity and avoids locking in losses during downturns.

Managing sequence-of-returns risk

‘Catch-all’ figure issues

Balancing spending and saving in retirement

“There’s a lot of psychology that goes around entering into retirement,” continues Squirrell. “One of the hardest things is talking to people, who have been savers all of their life, into becoming spenders. “When you stop work, or as you phase out of work, allowances may become available that were not available while you’re working such as the savings allowances.” He advises designing portfolios that take advantage of tax wrappers and exemptions. “Making sure that your savings portfolio is designed so anything that’s outside what I would call tax efficient wrap, so anything beyond ISAs and pension, you’re looking to utilise your allowances such as savings allowances, such as the dividend allowance, such as the capital gains annual exemption allowance.”

Strategies for non-linear retirements

“There has to be some flexibility,” says Squirrell. “Flexibility in terms of what can be done with the investments but also in terms of what can be done in terms of drawing income.” “For example, if I want to give up work at 60, my state pension does not kick in for seven years – that in itself is a non-linear approach.” In such cases, he suggests clients may need to draw more income early on and adjust later when other income sources begin. Rather than drawing taxable pension income immediately – which can trigger the Money Purchase Annual Allowance (MPAA) and restrict future contributions – he suggests retirees may want to access the tax-free elements of the pension, “whilst allowing the rest to continue to grow and not preventing further contribution.” Blended solutions offer another level of adaptability. “If I did buy an annuity within a drawdown arrangement, then I’d have the ability to flex the income and deal with the taxation,” he explains. “The one thing to not dismiss is the power of blending the two – blending guarantees with the flexibility.” “A high percentage of people want guarantees of income but almost the same percentage of people want flexibility. It doesn’t have to be binary.”

Using blended income sources

Squirrell highlights the value of accessing different types of assets to meet shifting income needs. “Having different options in terms of meeting your income needs is quite important – cash in the bank, ISAs, investment accounts,” he says. Utilising non-pension assets can help manage tax efficiently while maintaining flexibility. Investment bonds or general investment accounts may be suitable in the early years of retirement, particularly if phased alongside pension drawdown. To reflect changing retirement journeys, there are also new innovative investment strategies available in the market, such as the Standard Life Smoothed Return Pension Fund and the Standard Life Guaranteed Lifetime Income plan. Options such as these are designed to provide less short-term volatility while investing and a regular guaranteed retirement income for life but at the same time offering greater flexibility. The 4% rule remains a useful reference point but individual needs, market dynamics, and evolving retirement behaviours demand a more personalised, flexible approach.

“There has to be some flexibility in terms of what can be done with the investments but also in terms of what can be done in terms of drawing income”

“When you stop work, or as you phase out of work, allowances may become available that were not available while you’re working such as the savings allowances”

Read more from Fidelity on creating retirement income for your clients.

Changing policy, regulation, markets and client goals create ever-shifting sands, but also underscore the value advisers can bring. Technology, AI and new propositions are enabling more adaptive retirement advice

Retirement is increasingly understood as a journey rather than a single cliff-edge event. Clients can’t copy their parents’ path; yesterday’s defined benefit pensions and stable rules have given way to defined contribution pots, longer lifespans, increased cost of living and market volatility. Even newly-minted plans are being redrawn as pensions policy shifts. The complexity is stretching advisers, but many relish the intellectual challenge it brings, as well as the growing demand for advice and the value of planning.

One adviser shared a favourite outcome: “A factory manager came in, very stressed out. He’d built up pension assets and had a small inheritance, but he hadn’t done any art, his passion in life, for nearly two decades. Using a cashflow tool and a conservative plan, we could show him that his defined benefit and state pensions would cover most income needs, and his invested assets could comfortably fill the gap. He retired, completed an art degree, and he’s now an artist, making about a grand a month. He even painted me a picture of the bench where I proposed to my wife.” It’s a neat illustration of planning as confidence, not just compliance. Intergenerational planning is also shifting. Inheritance Tax announcements and policy noise have pushed wealth transfers up the agenda, with over half of advisers reporting rising demand.

Heather Hopkins Managing Director and Founder of NextWealth

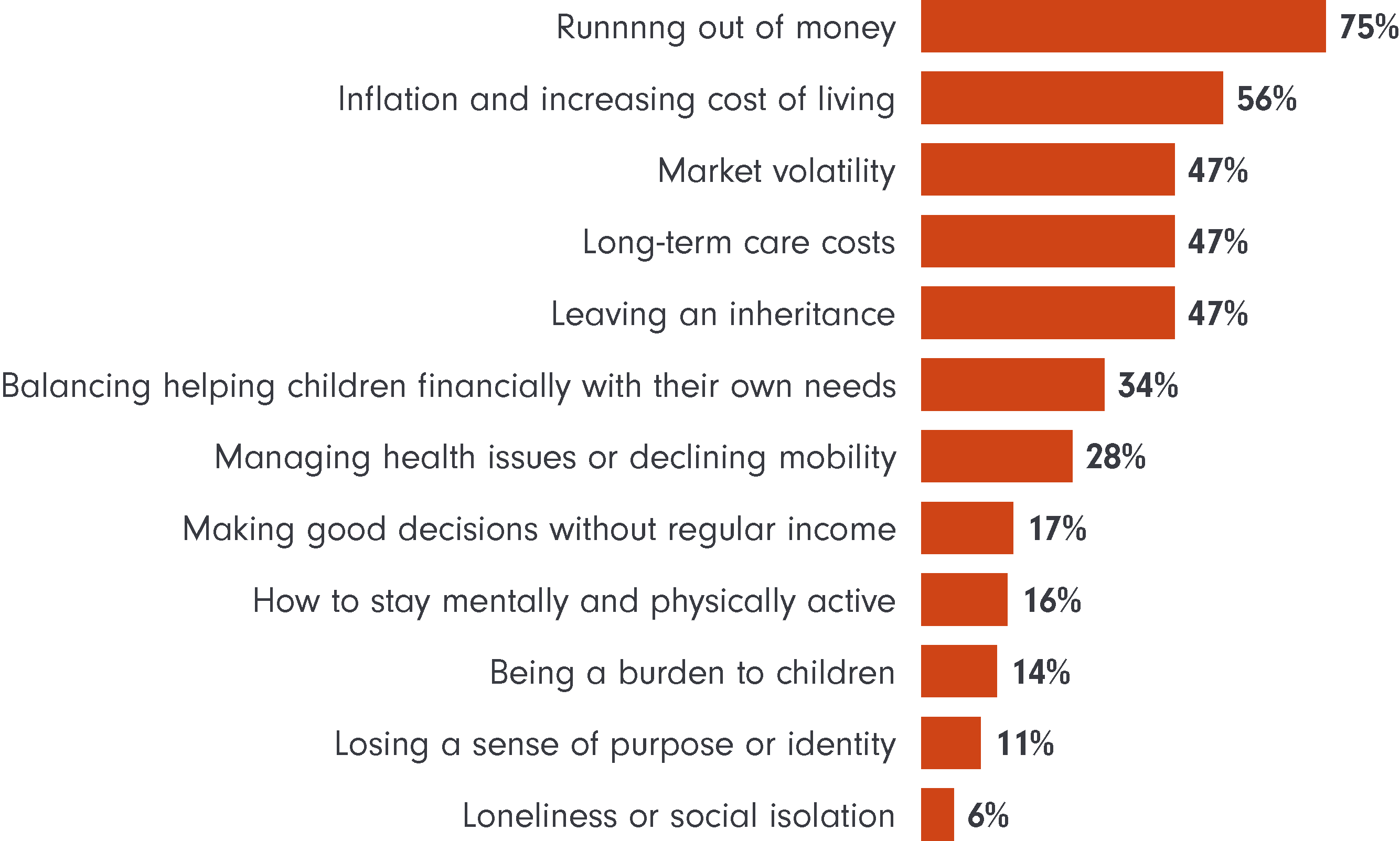

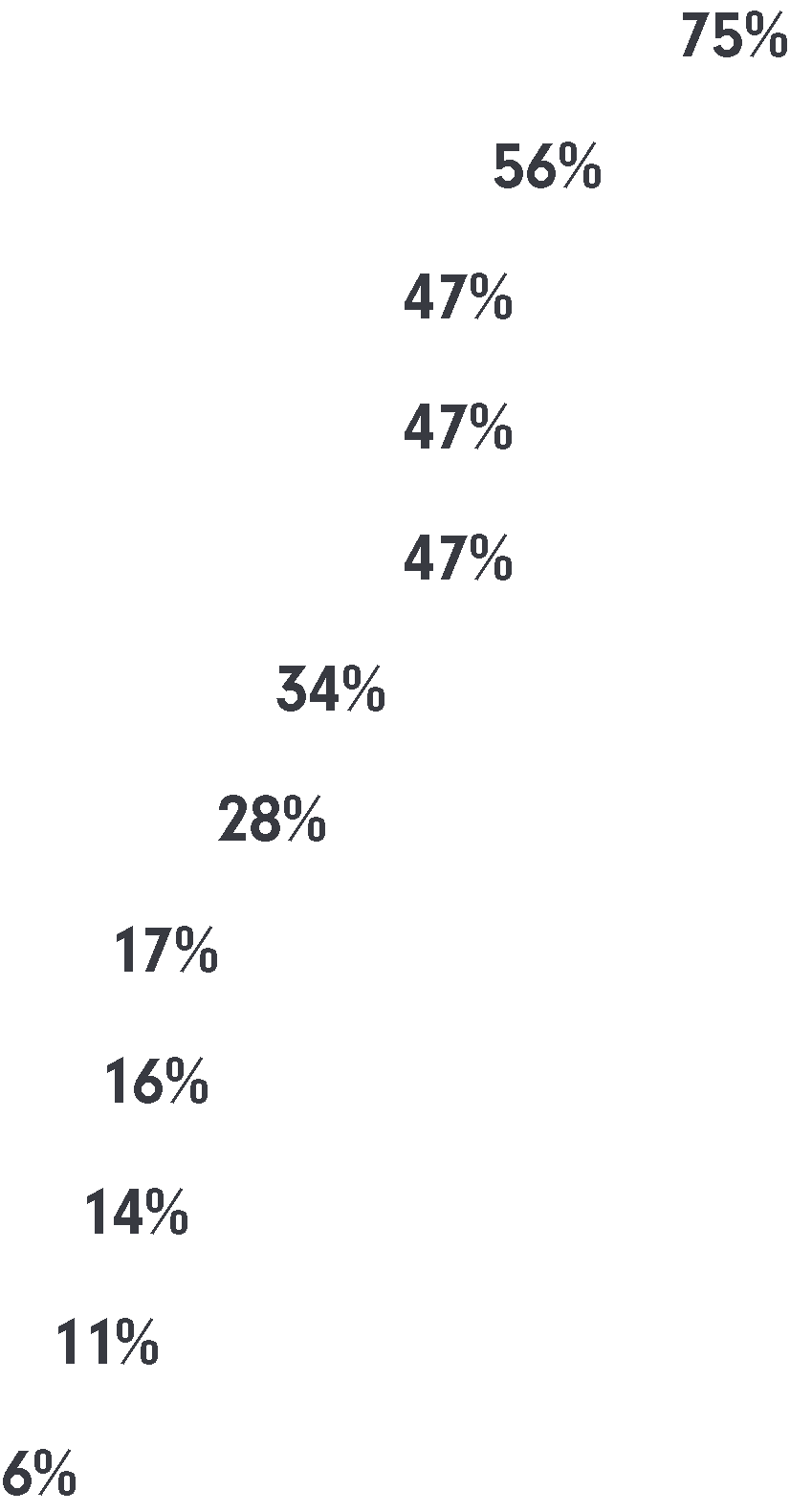

Technology is an enabler of this agility: cashflow tools let advisers stress-test plans, model trade-offs and visually demonstrate the impact of decisions. AI is moving from experiment into practice. Nearly one in five advisers (19%) implemented an AI tool in the past year, most commonly for meeting notes and summaries - freeing capacity for time with clients. Some firms are experimenting with AI to analyse communications, spot behavioural patterns and flag potential risks to income or investment outcomes. Uncertainty continues to dominate client conversations. Three-quarters (75%) of advisers report that clients approaching or in retirement are primarily concerned about running out of money. Yet advisers are often working with clients who are ‘under-living’ rather than over-spending. To address this, firms are leaning on modelling and visualisation tools to translate abstract scenarios into decision-ready insights.

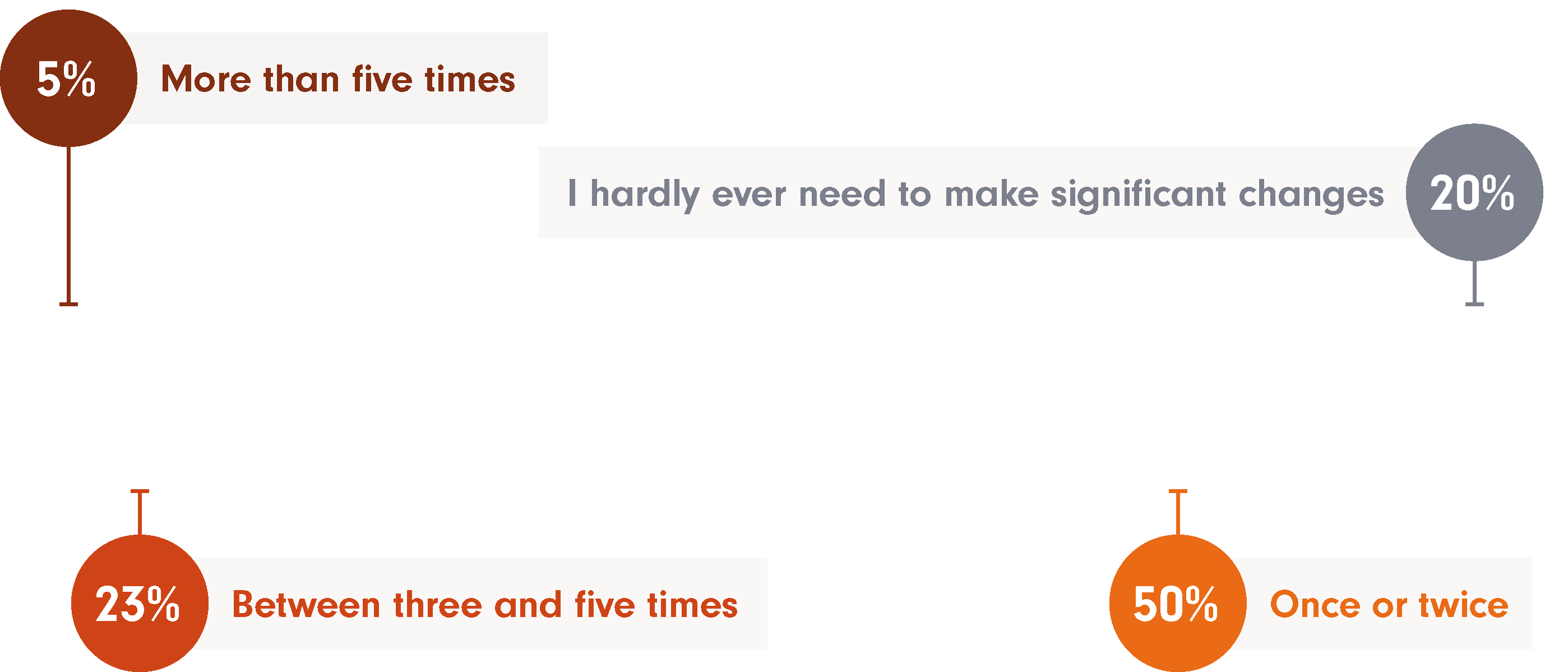

“Our IFA DNA data underline the dynamic nature of today’s retirement planning. More than three-quarters (78%) of advisers say they make significant changes to clients’ financial plans during retirement”

Read more from Fidelity's IFA DNA research.

Important information Issued by Financial Administration Services Limited, authorised and regulated by the Financial Conduct Authority. Fidelity, Fidelity International, the Fidelity International logo and F symbol are trademarks of FIL Limited. UKM1025/404983/SSO/1026

One retirement planner commented: “I have that technical speciality around pensions, but the bit I love is the planning. People come in asking, ‘Do I do this or that with my pension?’, but the real question is often, ‘why do you still want to keep working’? Sometimes the advice is the simple bit; the challenge is helping them see what life they want.” In this case, a client who was financially able to retire struggled to let go of the security of work. A phased step-down to one day a week helped build confidence. Our IFA DNA data underlines the dynamic nature of today’s retirement planning. More than three-quarters (78%) of advisers say they make significant changes to clients’ financial plans during retirement. Set-and-forget has given way to ongoing course correction as tax, regulation, markets and client goals move.

Significant changes typically made to a client’s financial plan over the course of their retirement

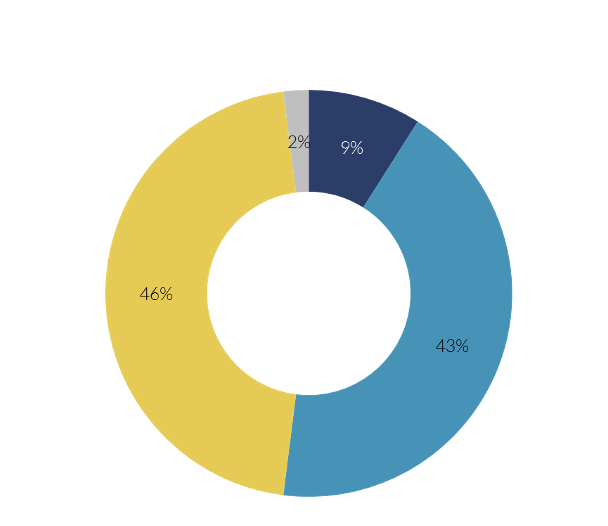

Client concerns in or approaching retirement

Change in demand for wealth transfer over the last 12 months

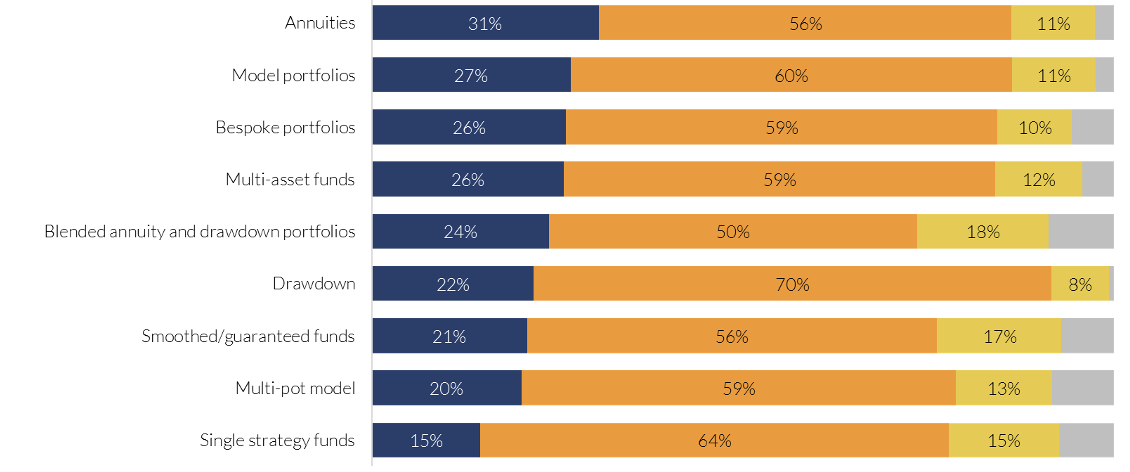

But younger clients don’t always want a traditional experience. Forward-thinking firms are responding with new propositions and clearer, bite-sized communications: meeting next-gen clients where they are and building relationships that last beyond the transfer event. This financial planning firm holds an annual educational event: “We’ll send a message out to our clients and say, ‘we’re putting on a session in our offices, we’ll provide pizza and drinks, send your kids along and we’ll chat through what a pension is, how to budget’. We’ll pick some topics that are relevant for them.” On income strategy, sentiment is evolving. Despite a sharp fall in advisers recommending annuities to all or most clients (down from 33% in 2024 to 10% in 2025), nearly one in three (31%) plan to increase annuity use over the next year. The direction of travel is towards blended strategies: maintaining drawdown flexibility while using partial annuitisation to lock in a base level of certainty. In a choppy environment, many retirees value predictable income that shields them from market swings and behavioural missteps.

Expected change to recommended investment strategy over the next 12 months

Annuities

Model portfolios

Bespoke portfolios

Multi-asset funds

Blended annuity and drawdown portfolios

Drawdown

Smoothed/guaranteed funds

Multi-pot model

Increase

31%

56%

11%

27%

60%

26%

24%

22%

21%

20%

15%

59%

50%

70%

64%

10%

12%

18%

8%

17%

13%

No change

Decrease

N/A

Single strategy funds

43%

46%

9%

2%

Yes, there has been a significant increase

Yes, there has been a slight increase

Don't know

The real value in retirement advice is human understanding. Four adviser archetypes lean into different strengths to know clients well, but time is squeezed by routine tasks and compliance. Used well, AI and automation free capacity for deeper conversations, and for the small but vital follow-ups and check-ins that clients remember

Advisers also tell us that extra time unlocks the “nice-to-haves” that clients really value. “Phoning when a pension transfer lands: ‘You did the paperwork two weeks ago; it’s in and invested now.’ That’s what clients remember. If you asked them about value, many would say, ‘It was lovely they called, rather than me just getting a notice.’”

Our research points to four distinctive leanings - what gives different advisers the most meaning and where they want to spend time. The Relationship-Builder is at their best in long, trust-rich conversations but currently furthest from their ideal day because admin crowds out client time. “If all I had to do was look after my clients, I’d be very happy… but a two-hour client meeting becomes three or four hours of writing up and checks.” In retirement advice, they excel at uncovering the real brief - the life change beneath the pension question. “A client who's in front of me, they're coming for a reason, which is typically pensions. I want to move them to a better place. Just to open their eyes and say, ‘hey, this is what we could do’.” What they need most are tools and workflows that reduce paperwork and create space for understanding their clients more deeply. All advisers are problem solvers, but the Complex Problem-Solver thrives on knotty, multi-factor cases. In retirement planning, they’re the architects of blended strategies and stress tests.

Four ways advisers create value

What clients feel as value

AI to win back client time

AI can help. Tools for meeting transcription, note generation and first-draft reports are already in use; 19% of firms added an AI tool in the last year, and 40% of advisers think AI will let them spend more time with clients. AI and technology’s role is to augment the human side of retirement advice, not replace. One firm is tackling early nerves by asking teams to ponder: “What would you have the robot doing and where would you like to focus more care and attention and your empathetic side that a robot wouldn’t have?” Automation can go beyond routine admin to surface insight that complements human judgement, suggesting financial personality cues, flagging behaviour shifts (unusual withdrawals between reviews, for example), and spotting patterns in communications so advisers know when to check in. Humans still own the tone, framing and recommendations; technology’s role is to shorten the path to a better conversation.

“Advisers also tell us that extra time unlocks the “nice-to-haves” that clients really value”

“The outcome we’re all aiming for in retirement advice is the same: clients who understand their choices, feel supported through change, and leave each conversation a little more certain about the road ahead”

Important information Issued by Financial Administration Services Limited, authorised and regulated by the Financial Conduct Authority. Fidelity, Fidelity International, the Fidelity International logo and F symbol are trademarks of FIL Limited. UKM1025/415232/SSO/1026

Advisers love the client work, but their diaries don’t. Our latest IFA DNA research shows practitioners spend only a third of their time with clients; the rest is swallowed by report writing, compliance and admin. Unsurprisingly, 72% say reducing admin would most improve their workday, and 66% want more in-person meetings. With limited face time, the process protects advice quality: a well-run review cycle, documented suitability, clear MI, and robust file checks. But depth of understanding, the “why” behind a client’s choices, comes from time. More time lets advisers surface unspoken fears and test trade-offs, particularly valuable at retirement when decisions are emotionally complex.

The Educator/Empowerer gets their energy when clients truly understand. “I want them to feel they’ve understood it, not just trusted me.” The retirement conversation centres on the educational, with visual scenario tools, plain-English follow-ups and short, repeatable explainers to help turn complex retirement trade-offs into those “I get it” moments. The Tech/Strategy Implementer balances client work with process improvement. In retirement advice, they make the whole engine smoother so colleagues can spend more time where judgement matters. The right blend of process, people and technology creates room for all the different archetypes to lean on their particular strengths. The outcome we’re all aiming for in retirement advice is the same: clients who understand their choices, feel supported through change, and leave each conversation a little more certain about the road ahead. As one financial planner told us, “That’s what stands us out from the next guy down the road, because at the end of the day, we’ve all got the same box of tricks. What stands us out is what the client feels about you as a person and vice versa.”

In this Q&A, Mana Jhaveri, a Behavioural Scientist at Cowry Consulting, discusses retirement research conducted with Fidelity Adviser Solutions. The research explores attitudes toward retirement and identifies the psychological barriers and drivers that influence an individual's readiness gap for retirement

Mana Jhaveri Behavioural Scientist at Cowry Consulting

1. What are people's general attitudes towards retirement planning and how could this impact retirement readiness?

People have a number of different attitudes to retirement planning, and most are negative. Firstly, worry is very common in the pre-retirement stage, and this is usually linked to people being afraid of not having enough resources and uncertainty about future income. Secondly, individuals can sometimes fear approaching financial advisers due to something known as financial adviser anxiety. This is the fear of being judged due to inadequate savings or a lack of financial knowledge, which can then deter them from speaking to an adviser. Thirdly, people experience identity shifts at retirement. This can be especially acute for those who draw a lot of their identity from work. Retirement represents a loss of their work identity, which can be challenging. On the other hand, people who enjoy planning and have clear goals in mind tend to feel more prepared for retirement. This group is more likely to engage with advisers, accumulate savings and engage in the positive behaviours that prepare them for retirement.

“A good adviser and client relationship is a significant predictor of psychological retirement readiness”

Read more from Fidelity on the psychology of retirement.

“People who enjoy planning and have clear goals in mind tend to feel more prepared for retirement. This group is more likely to engage with advisers, accumulate savings and engage in the positive behaviours that prepare them for retirement”

2. What factors other than wealth play a role in retirement readiness?

Apart from wealth, client knowledge is the strongest driver of readiness. Known as financial self efficacy, a client's financial literacy, (how well they understand financial concepts) and their confidence in applying that knowledge and using it to make decisions about their future finances, is a strong predictor of retirement readiness.

Based on a psychological framework called the Theory of Planned Behaviour, we can put key influences into three buckets. The first bucket is control and it's the most important. Our findings show that the need to feel in control of your retirement and to have the capability to plan for it are strong predictors of feeling psychologically ready for it. The feeling of agency and control comes partially from enjoying the retirement planning process, which then ties into a sense of confidence and emotional satisfaction which can help people feel ready.

3. What are the key social, emotional, and behavioural forces that could influence retirement readiness?

The theory of planned behaviour (TPB) is a social psychology theory that predicts behaviour based on an individual's intentions, which are influenced by three main factors: attitude, subjective norms, and perceived control.

The second bucket is attitude. We know that there are some negative attitudes when it comes to retirement, particularly around the fear of getting bored or losing a sense of purpose. The final bucket is social norms. People are really affected by those individuals around them who are important to them. The influence of friends and family is positive if they are also in the same stage in life. However, if individuals are worried about leaving an inheritance or have concerns about becoming dependent on their family, these worries can have a negative influence on retirement readiness.

4. What are some predictors of psychological readiness and how do retirement goals, beyond money, help people become ready for retirement?

A good adviser and client relationship is a significant predictor of psychological retirement readiness. This suggests that there are a lot of things in an adviser's control which can contribute to clients feeling more ready for retirement. Apart from that, we also know that an individual’s financial self-efficacy is also a significant predictor. An adviser who can educate and empower their clients to feel more in control of the retirement journey can help them feel more psychologically ready. Retirement goals beyond money can also help people feel more prepared for retirement. Individuals who are able to visualise their purpose and lifestyle in retirement from a more practical and experiential point of view tend to have a stronger ability to plan for those goals.

5. The world can feel very uncertain right now with policy tax changes, volatile markets, high inflation in the UK and more. How could advisers approach clients who have worries about issues that may be out of their control?

Transparency, acknowledging uncertainty and talking about what is making people anxious is very important. Communicating regulatory and market changes proactively to clients and showing expertise and due diligence are important in building and maintaining trust. Advisers should reassure clients that they are there to tread the stormy waters with them, both now and as they prepare for retirement.

“A fundamental shift” is set to change how retirement plans are put together, with annuities potentially entering a new era of relevance

Earlier this year government confirmed that, from 2027, most unused pension funds and death benefits may fall under the scope of Inheritance Tax (IHT). HMRC anticipates this will generate £1.46bn in tax receipts from 2029/30, and “remove distortions” that it argues that have led to pensions becoming increasingly used as tax planning vehicles to transfer wealth. There is time to prepare clients’ financial plans for this, but Paul Squirrell – head of retirement and savings development at Fidelity Adviser Solutions – says this poses a “fundamental shift” in how advisers will operate. “It's a fundamental shift from what advisers have been doing for the last 10 years,” says Squirrell, referring to the period since pensions freedoms and how this altered savers’ views on pension extraction. “It’s important we don't lose sight of the benefits of saving into pension arrangements as a result of the recent IHT changes, but you're going to have to have a strategy for spending that money during retirement.”

Any change around taxation will naturally concern most savers, but this latest IHT development is likely only going to impact those with excess savings and who do not exhaust the majority of their pension funds during retirement. However, for people in this situation there will be a heightened need for more concise retirement planning. This is likely to be exacerbated by longer life expectancies which will require more people to consider not only their income provisions for retirement but how they potentially work with what’s left. Squirrell sees this creating a need for more concise cashflow modelling and expense forecasting services from advisers, with clients keen to develop a granular picture of what their retirement will look like. This is also likely to spark conversations across the wider family and friends, impacting anyone who could be a beneficiary of an individual’s estate. “This is probably the biggest thing - it's undoubted that these changes are going to accelerate the inter-generational wealth transfer,” says Squirrell. “In the past you could have left the money in pensions but more people are going to want to consider gifting during their lifetime. It's going to be a challenge for advisers and providers alike to consider the wider family.” Regardless of individual circumstances, it’s clear that this change will further enhance the need for advice. People will naturally want to know what this means for them, their families and, critically, if they need to start doing anything differently in preparation for 2027 with big decisions to be made around gifting and wealth transfer. Squirrell adds: “There’s no right or wrong answer, but it's a discussion that maybe people wouldn't have had before the changes came in a year ago.” The changes are expected to apply to deaths on or after 6 April 2027.

Preparing for impact

A role for annuities

With advisers looking to re-evaluate their clients’ financial plans, a lot of tools and products will receive fresh attention. Annuities have already become increasingly popular, largely due to increased rates, but there is a growing argument that these can play a bigger role in a future where unused pension funds are taxable. “If pensions are going to become your primary vehicle for funding for your retirement, then it naturally follows that you're probably going to look at things such as annuities,” says Squirrell. Here, he sees annuities as becoming useful for income generation, thereby easing pressure on pension funds and allowing this money to be used differently as part of a wider financial plan. “I don't think anyone would buy an annuity just to give away the capital to get rid of an inheritance tax liability,” adds Squirrell. “But if they can secure a guaranteed income that covers essential and maybe a bit more needs, then maybe that means they can be more concise and proactive with capital planning elsewhere.”

“It’s important we don't lose sight of the benefits of saving into pension arrangements as a result of the recent IHT changes”

Read more from Fidelity on technical matters

Important information The value of your clients' investments and the income from them, can go down as well as up, so they may get back less than they invest. Tax treatment depends on individual circumstances and all tax rules may change in the future. Withdrawals from a pension will not normally be possible until an individual reaches age 55 (57 from 2028). This information is not a recommendation for any particular investment. Issued by Financial Administration Services Limited, authorised and regulated by the Financial Conduct Authority. Fidelity, Fidelity International, the Fidelity International logo and F symbol are trademarks of FIL Limited. UKM1025/415245/SSO/1026

“More people are going to want to consider gifting during their lifetime. It's going to be a challenge for advisers and providers alike to consider the wider family”

Sequencing risk remains a major threat to retirement portfolios, but the traditional strategies used to combat it often come with a cost. However, a strategic balance can be found by managing multiple strategies within a single pension

The threat of sequencing risk in retirement portfolios has prompted the development of various strategies to combat this danger. While each approach may be appropriate in the right circumstances, advisers should recognise that protection often comes at a cost, whether through performance drag or withdrawal restrictions.

Living off natural income or yield. Clients use the interest, dividends and income generated by their fund and withdraw this each year. The obvious disadvantage is that income is likely to vary year by year. In addition, the search for income may cause unintended bias when selecting investments Fixed percentage of the fund. A variation is to take a fixed percentage of the fund value each year (as opposed to a fixed percentage of the initial fund value). Again, income can rise and fall from year to year. Rising equity glide path. This involves starting with a low exposure to equities, usually between 20-40%, rising over time to between 40-80%. However, if markets rise during the early years, there is an opportunity cost. Cash bucket. A further approach is to hold a cash buffer. This usually involves dividing the fund into sub-funds or ‘buckets’, typically cash, bonds and equities. The cash bucket might equate to 2-3 years income to ride out market falls.

Traditional approaches and their trade-offs

Case study: Achieving balance

Consider a 65-year-old with a £500,000 fund planning to take an income of £20,000 each year. Using annuity rates as an example, a single life, level annuity purchased with £200,000 would currently provide over £15,000 per annum. That means the client would only have to withdraw a little over 1.5% from the remaining fund to meet their income target. This is based on a level annuity, so inflation protection would need to be provided by the remaining fund. In this example, 40% of the fund is used to buy a guaranteed lifetime income and 60% is invested in equities. Bonds could be added to aid diversification and provide additional flexibility. What if we take a slightly different approach, using 20% of the fund to buy an annuity, investing 20% in bonds and the remaining 60% in equities? Again, using annuity rates as a proxy, single life, level annuity rates at age 65 provide around £7,800 per £100,000 purchase price, leaving £12,200 to be found from the remaining fund. This means just over 3% still needs to be withdrawn from the invested assets. This could leave the client still exposed to some sequencing risk, though adding a small cash reserve could mitigate this, or income could be strategically taken from the bond element, assuming a negative correlation with equities. A further refinement could be to add a smoothed managed fund, which provides an alternative source to make up any shortfall if bonds and equities are positively correlated. When markets fall, the value of the fund may fall, but by less than the actual movement in the price of the underlying assets.

“Advisers should recognise that protection comes at a cost, whether through performance drag or withdrawal restrictions”

Read more about Fidelity’s Flexible Investment and Retirement Solutions

Issued by Financial Administration Services Limited, authorised and regulated by the Financial Conduct Authority. Fidelity, Fidelity International, the Fidelity International logo and F symbol are trademarks of FIL Limited. UKM1025/415246/SSO/1026

• • • •

Calibrating the real threat

Given these trade-offs, we need to ask: how worried should we be about sequencing risk? Historical evidence suggests that significant market falls without a relatively quick recovery are rare. US data shows that the average length of a bear market is about 9.6 months. Since 1945, there have been 15 bear markets, working out to roughly one every five years. This suggests that over most time periods, markets rise. The implication is that holding excess cash or reducing equity exposure may detrimentally impact performance over the long term. The question then becomes whether there are strategies that might produce better long-term outcomes while still protecting against sequencing risk. There is growing evidence that including a guaranteed lifetime income within drawdown could achieve this balance.

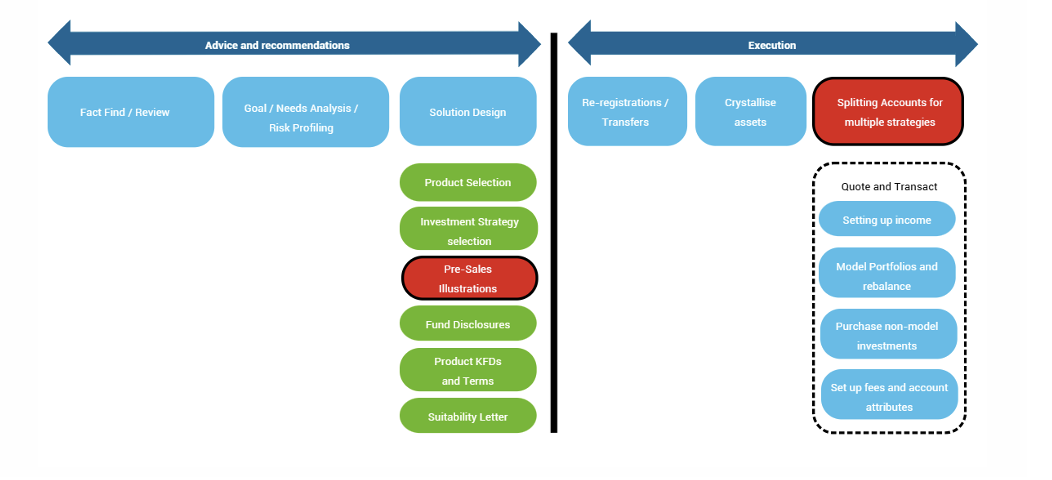

Tailored, integrated solutions for different retirement needs

Clients will invariably have a range of needs or goals. Retirees may require an immediate income from their pension but may also need some of their savings to cover potential expenditure in the future, such as health and care costs. Separately, if the client wishes to pass on some of their wealth to loved ones, then the pension may need to fund this too. As a result, it may be appropriate for pension assets to be divided into different accounts – each with a different purpose that require different investment approaches. Fidelity Adviser Solutions’ new Flexible Investment and Retirement Solutions facility provides a simple and straightforward way to manage multiple strategies within a single pension. It allows advisers to create and maintain any number of separate accounts for a client – for both pension savings and pension drawdown.

An example of how the service works

In this example, four separate accounts can be created by the adviser – one to generate pension income, another to hedge against market volatility, with two further pots to account for medium and long-term needs – with each account adopting a different investment strategy.

Other benefits to this strategy:

Different investment approaches can be used in each account, including advisers’ own model portfolios, models from one of more DFM or individually selected investments. In addition, distributions could be set to distribute to cash for say the short to medium investments and to reinvest for longer term strategies. Regular savings can be funnelled into one or numerous accounts, also available for ISA and investment accounts. Assets within each account can be transferred to other pots as client needs change over time. Separate settings can be applied to each account, such as the rates for adviser and DFM fees. To support the advice process, standalone pension pre-sale illustrations can be produced for each client.

• • • • •

Supporting the advice process

To fully support the advice process and the need to provide a pre-sales illustration, we have introduced a new standalone pre-sales illustration tool. This tool allows you to illustrate the end state you are recommending to a client.

Taxable Pension Income

Drawdown Arrangement

Goal

Investments

Pension Income

Volatility Hedged Returns

Medium Term

Long Term

Cash, Guaranteed Lifetime Income

Non-Model based Based Assets including Smoothed Funds

Balanced Risk DFM Model Portfolio

Adventurous Risk DFM Model Portfolio

Account

Stock transfers: Move cash and investments and create new accounts if required

Fact Find / Review

Goal / Needs analysis / Risk profiling

Solution design

Re-registrations / Transfers

Crystalise assets

Splitting accounts for multiple strategies

Product selection

Investment strategy selection

Pre-Sales illustrations

Fund disclosures

Product KFDs and terms

Suitability letter

Setting up income

Model Portfolios and rebalance

Purchase non-model investments

Set up fees and account attributes

Quote and Transact

Advice and recommendations

Execution

Funding a comfortable retirement is a challenging prospect. There are several moving parts to navigate in order to successfully help clients manage their finances, often interrelated and at times conflicting. Retirement has also changed from what it has been historically, with longer life expectancies, rising care costs and a move towards more fluid employment arrangements. This all means retirees require more from the funding solutions they rely on for this part of their lives. This calls for skilful management of many variables that can easily derail a client’s retirement plans if not reviewed regularly. A key one of these is sequencing risk, which can potentially have devastating impacts on the remainder of a saver’s retirement. A range of strategies have been developed to combat this, but they can potentially impact the long-term aim of maximising returns for a given level of risk. These may include reducing equity exposure in the early years or holding significant cash reserves. Alternatively, there are strategies that vary income, which may be impractical. Everyone’s different and there is no one universal solution for all. However, a previously overlooked approach is now gaining traction that is championing two polar opposite yet attractive components of retirement funding.

The best of both

The benefits of integration

Flexibility and certainty are both valued by people approaching retirement. An integrated approach can provide both: combining the certainty of a guaranteed income for life with the flexibility of drawdown, while delivering better outcomes in many circumstances. This strategy can also help combat sequencing risk without the need to hold a significant cash bucket, reduce equity exposure substantially or vary income from year to year. Additionally, there are tax advantages to be gained from integrating a guaranteed income product into a drawdown solution. For instance, if the income isn’t needed at any point, it can simply be added to the drawdown pot. Assuming the income payments aren’t required, they would be added to the fund without income tax being levied. There is also the option to choose value protection at the outset under a guaranteed income for life solution. On death after 75, this could be payable as a regular income, which may be taxable at a lower rate than would be the case if death benefits were payable from a separate annuity (the treatment of death benefits is set to change from April 2027, however). Advisers are spoilt for choice when it comes to retirement strategies for their clients, and these will all depend on the latter’s specific situations. Fundamentally it’s important to recognise that retirement is no longer a single point in time but a journey that requires ongoing flexibility. With Fidelity’s Flexible Investment and Retirement Solutions, advisers now have the enhanced toolkit they need to respond to these challenges and deliver secure, sustainable outcomes.

“Retirement solutions that integrate certainty with flexibility are attracting more attention as a way of navigating the decumulation challenges advisers face”

Read more on strategies to help your clients prepare for retirement

Retirement solutions that integrate certainty with flexibility are attracting more attention as a way of navigating the decumulation challenges advisers face. These ideals are different to one another but can work in tandem. This is likened to the complementary colour phenomenon, when a pair of colours that contrast actually both appear brighter when placed side-by-side. Similarly annuities and drawdown are polar opposites in many way, but in combination can mitigate each other’s weaknesses and bolster each other’s strengths. Including guaranteed lifetime income within a drawdown portfolio has traditionally been viewed as a method of covering essential expenditure. Though this may have little application for wealthier savers, for whom such expenses are a smaller proportion of their outgoings, regardless there are other reasons to include a guaranteed income for life. These include the peace of mind and happiness that comes from knowing that a regular guaranteed income is payable into perpetuity.

Fidelity’s Flexible Investment and Retirement Solution was designed to champion this approach, providing a simple and straightforward way to manage multiple strategies within a single pension. This allows advisers to efficiently create and maintain any number of separate accounts for a client, helping plan outcomes tailored to their differing needs and goals. There is a growing body of evidence that demonstrates including guaranteed income for life within a drawdown portfolio can deliver tangible results: better outcomes by way of a higher sustainable withdrawal rate and/or greater benefits on death. This can also help combat the insidious impact of sequencing risk, reducing the amount that needs to be realised from other assets.

Income payable throughout life Level of income not dependent on markets Guaranteed income for dependants Death benefits fixed at outset

Potential for growth Option to vary regular income Ad hoc withdrawals at any time Full fund value available on death

CERTAINTY

FLEXIBILITY

Complementary colours

The journey to retirement is not solely a financial one; it's deeply intertwined with a client's psychological readiness. For financial advisers, navigating this complex landscape – addressing both the tangible and emotional aspects of retirement – is key to shaping clients’ futures

Research from Fidelity Adviser Solutions and Cowry Consulting into retirement readiness reveals that while having sufficient finances is the strongest driver of a client's peace of mind in retirement, having a strong financial adviser-client relationship acts as a crucial "highway" between the two. "A significant portion of peace of mind in retirement is not just about numbers, but about building trust. Reassurance and guidance from the adviser in turn helps clients feel more ready for retirement," says Mana Jhaveri, Behavioural Scientist, Cowry Consulting.

“A good adviser and client relationship is a powerful predictor of psychological retirement readiness”

Learn more about the psychology of retirement

Practical strategies for engagement

Jhaveri outlines actionable strategies that advisers can use to narrow the retirement gap. Concretisation People may struggle to act on abstract information and concretisation is a technique to help make abstract concepts more tangible, often by helping people visualise outcomes in a clear and concrete manner. Advisers have access to cash flow modelling tools which show clients how their finances can evolve over time. Helping them visualise scenarios turns complex information into something that feels more actionable and tangible. The more information that advisers can get from clients to plug into the tool, the better they can help them visualise retirement scenarios. Authority bias People tend to place more trust in people who they perceive as experts in the field. Clients are really looking to advisers to be that trusted expert and a source of reassurance. Just simple actions like sharing credentials, experience, number of years in practice and success stories, helps elevate authority and signals credibility. Mental accounting People naturally divide money into separate mental accounts in their minds. For example, they have different accounts in their brains for savings, holidays and inheritance. In retirement, people need finances for multiple goals, like lifestyle, healthcare, legacy and others. Clients might be thinking about these separately, rather than as one pool. Advisers can help here by creating distinct pots for different goals, which then helps planning feel more intuitive, manageable and aligns with how people already conceptualise their finances.

A strong, supportive relationship explains around 26% of the psychological readiness gained from financial readiness.

Proactive engagement

It's no surprise that due to the complexity and planning around retirement, clients can feel disconnected from the process. The research shows that as they near retirement, some older clients tend to feel less engaged with their advisers and may have the knock-on effect of feeling less ready for retirement.

The ability of advisers to provide peace of mind during the retirement transition is crucial and those advisers who are transparent and able to provide reassurances are more likely to build stronger, more trusting relationships. People are more likely to trust those that they feel are like them. For advisers, this means taking the time to find common ground with the client, demonstrating that they share similar values and building that rapport on a more human level.

Humans are inherently present-focused, so we find it difficult to picture, empathise and connect with our future selves. Advisers who are working with younger clients, can have a tough time bringing the retirement proposition into the present. Saying that younger clients need to save £1,000,000 for retirement feels very daunting. Instead, advisers should break financial goals down into easier steps. For example, setting smaller savings targets that are framed in the present day (eg: save 2% of income every month) can be effective strategy for this. Additionally, automating savings is a powerful mechanism for overcoming procrastination and inertia—key behavioural challenges that often prevent clients from reaching long-term financial goals." Therefore, such smaller, automated steps can be powerful for younger clients who find it challenging to plan and think deeply about retirement at 60, when they are in a stage of life where they are saving for the next holiday.

Gen Z clients: Bridging the empathy gap

“We think it's because the closer they get to retirement, the larger it looms, and this can often make people more anxious. That tends to trigger avoidance behaviours, where an individual may bury their head in the sand because it feels too big," says Jhaveri.

It's important for advisers to be aware of client needs at this age and stage; and one of the ways they can do this is by initiating a more proactive engagement strategy.

"It requires a lot of handholding when people feel overwhelmed and when they don't know what to do. Advisers should make it as easy as possible for their clients to engage with them," says Jhaveri.

She says that co-creating retirement and inheritance plans with clients - rather than creating it for them - gives people more of a sense of ownership over their retirement plans and the confidence in their ability to succeed.

A good adviser and client relationship is a powerful predictor of psychological retirement readiness which indicates that there is a lot that advisers can do to contribute to a client's feeling of wellbeing leading up to and in this phase of life.

"The adviser who can educate and empower their clients and give them the skills to plan and budget effectively and help them feel more in control of the whole retirement journey, can help close the retirement readiness gap significantly," says Jhaveri.

Working in partnership with Adviser Home, this guide explores the broad picture of the changing retirement market. It considers different aspects of the challenges that both advisers and their clients face. It is also intended for advisers to use as a practical sense check of where their own advice processes are. It gives a brief overview of the many choices, options and retirement income sources there are available, including relatively new options such as smoothed pension funds and guaranteed lifetime income products within drawdown. View Report

View Report

Retirement advice: The way forward

In this report we look at the impact of different risk factors and how retirees could manage these to make the most of their retirement savings. View Report

How much does a comfortable retirement cost?

This report considers the options available if a shortfall is identified some years out from retirement. The most common options are saving more or retiring later. In the case of the former, which products are most effective? There are also other solutions available which can shore up retirement finances. As retirement draws near, we explore some of the challenges advisers and their clients might grapple with to achieve a comfortable retirement highlighting some of the FCA’s concerns. The report sheds light on some of the actions advisers can take to develop effective retirement strategies for their clients. View Report

Countdown to retirement

This report explores some of the potential pitfalls and issues that may arise during retirement planning processes. For many advisers, this report will be a checklist against which to validate their practices and processes. But none of us are infallible. It’s important that, collectively, we do all we can to prepare and protect clients at this critical stage of their life. View Report

Retirement planning – ten pitfalls to avoid

This report reviews some of the pros and cons of different approaches to dealing with sequencing risk and explores whether there may be better options. New solutions that can deliver optimal long-term outcomes, commensurate with the clients’ risk tolerance and capacity, without exposing clients to market falls in the early years. Of course, there’s no one strategy that’s right for everyone. Different strategies could all be appropriate in the right circumstances – depending on the individual client. View Report

The benefits of integrated solutions

In this report, we look to develop a deeper understanding of risk. How we assess risk? What shapes our view of risk? And which characteristics define our perspective of risk? Then we evaluate some of the options advisers could consider to manage risk during retirement and explore the advantages and disadvantages of different solutions. View Report

Investment risk and retirement

The FCA in its ‘Retirement income advice thematic review’ expressed concerns around sustainable rates of withdrawal. Where firms use a withdrawal guide rate, the FCA wants to ensure this takes account of individual circumstances. Many firms will be using cash flow modelling, which will take account of individual circumstances. This report provides a quick guide to the variables that determine a sustainable withdrawal rate and how these could be applied in practice. View Report

Sustainable withdrawal rates for drawdown clients

Inflation can have a profound impact on the finances of retirees. The obvious consequence is the erosion in the value of income over time, but inflation can have a far-reaching impact over many aspects of retirement. In this report, we examine crucial issues such as:

The impact of inflation on retirement planning

Is the inflation rate at the start of retirement potentially as damaging as sequencing risk? Should retirement income be fully protected throughout retirement? Given annuities are impacted by inflation, do increasing annuities offer value for money?

• • •

The word ‘unretired’ has recently entered the financial services lexicon. It’s used to describe people who’ve left the workplace to retire and subsequently decide to return to work. In this report we consider some of the implications of this seminal change in retirement and review the issues advisers should consider in developing solutions. We also look at a practical example to demonstrate how complex retirement planning can become. View Report

Reinventing retirement

There are a number of ways advisers can help clients navigate the perils of retirement, however it’s clear that no one size fits. In this report we review how the thinking around sustainable withdrawal rates has changed. We also explore which factors determine how much can safely be withdrawn and consider strategies advisers can use to mitigate the risks of running out of money. View Report

Help your clients survive retirement

Retirement these days is no longer a single event. The initial transition to retirement could involve several twists and turns and require regular reviews. This report looks at some of the issues that can arise and their possible impact. We’ve also included a checklist you can use to compare with your own process. View Report

The path through retirement

Here, I summarise the main points that affect financial planning. For my full analysis and comment on the Budget, please visit the Technical matters area of the Fidelity website.

“As announced last year, the government will bring most unused pension funds and death benefits into the scope of inheritance tax from 6 April 2027”

Important information The value of your clients' investments and the income from them, can go down as well as up, so they may get back less than they invest. This article provides information and is only intended to provide an overview of the current law in this area and does not constitute financial advice, tax advice or legal advice, or provide any recommendations. The value of benefits depends on individual circumstances. The minimum age clients can normally access their pension savings is currently 55, and is due to rise to 57 on 6 April 2028, unless they have a lower protected pension age. Different options may have different effects for tax purposes, different implications for pension provision and different impacts on other assets and financial planning. Issued by Financial Administration Services Limited, authorised and regulated by the Financial Conduct Authority. Fidelity, Fidelity International, the Fidelity International logo and F symbol are trademarks of FIL Limited.

ISAs

Pensions

As widely trailed before the Budget, the annual Cash ISA limit is to be cut to £12,000 from April 2027 (the remaining £8,000 can be invested in a Stocks & Shares ISA). However, this reduction will only apply to those aged under 65. Anti-circumvention rules will be put in place to prevent cash-like investments being held within Stocks & Shares ISAs.

The triple lock guarantee will see State Pensions increase by 4.8% from April 2026. The government also announced they will ease the administration burden for pensioners whose sole income is the basic or new State Pension so they will not have to pay small amounts of tax via self-assessment (any State Pension boosted by an increment will not qualify). This applies “for the remainder of the current Parliament”. From April 2029, pension contributions above £2,000 per annum made via salary sacrifice will be subject to employer and employee National Insurance (NI) Contributions. The government also confirmed well-funded defined benefit schemes can pay surplus funds to members over the minimum pension age from April 2027, where permitted by the scheme rules. As announced last year, the government will bring most unused pension funds and death benefits into the scope of inheritance tax from 6 April 2027. It was confirmed that personal representatives can instruct administrators to withhold 50% of taxable benefits for up to 15 months to cover potential inheritance tax.

Voluntary NICs

From April 2026, individuals will no longer be able to pay voluntary Class 2 NICs for periods spent abroad, leaving only Class 3 contributions (at £18.40 per week) as an option for those living overseas. Eligibility rules are also being tightened.

Personal taxation

The standard income tax personal allowance and national insurance threshold will both remain frozen at £12,570 until April 2031. In addition, the higher and additional rate thresholds will remain frozen at £50,270 and £125,140 respectively until 2031 for taxpayers in England, Wales, and Northern Ireland. The personal savings allowance and starting rate band for savings income also remain unchanged, as does the dividend allowance. Somewhat unexpectedly, the Chancellor announced an across the board 2% rise in the rate of income tax paid on savings interest generated outside of ISAs and pensions from April 2027. Therefore, the basic, higher, and additional savings rates will rise to 22%, 42%, and 47% respectively. Likewise, dividend tax rates will rise by 2% to 10.75% and 35.75% from April 2026. Property income will be taxed separately from April 2027, with the basic, higher, and additional rates set at 22%, 42%, and 47% respectively across England, Wales, and Northern Ireland.

Inheritance tax

The IHT rules were broadly left unchanged in this year’s Budget. However, the Chancellor announced the nil-rate band (£325,000) and residence nil-rate band (£175,000) will remain frozen until April 2031.

VCTs and EIS

The government announced the rate of VCT income tax relief will fall from 30% to 20% from April 2026. However, both the annual and lifetime investment limits for VCT and EIS schemes will double to £10 million (£20m for ‘knowledge-intensive companies’ or KICs). The company lifetime investment limit will also double to £24m (£40m for KICs). Both schemes have been extended to April 2035.

Summary

It is fair to say the run up to the Budget was a challenging time for those involved in financial planning. The positive for advisers and clients is it doesn’t appear anything has changed for those wanting to take advantage of pension and ISA allowances in the next tax year. Beyond pensions and ISAs, it’s always important to think about what other allowances can be used. Before considering whether to invest in collectives (General Investment Accounts), onshore, or offshore bonds, for example, it remains essential to consider all the variables and, of course, the client’s individual circumstances.

Fidelity's summary covers the key changes that matter for financial planning - ISAs, pensions, tax thresholds, inheritance rules, and investment reliefs. It also explores the tax implications across different client scenarios and wrappers for the current tax year as well as for changes coming in April 2026 and April 2027. View summary

Join Fidelity Adviser Solutions’ experts as they unpack the key Budget announcements and their practical implications for financial advisers. From pension planning opportunities and salary sacrifice changes to ISA restrictions and evolving tax rules, this discussion explores the key developments and what they could mean for you and your clients.